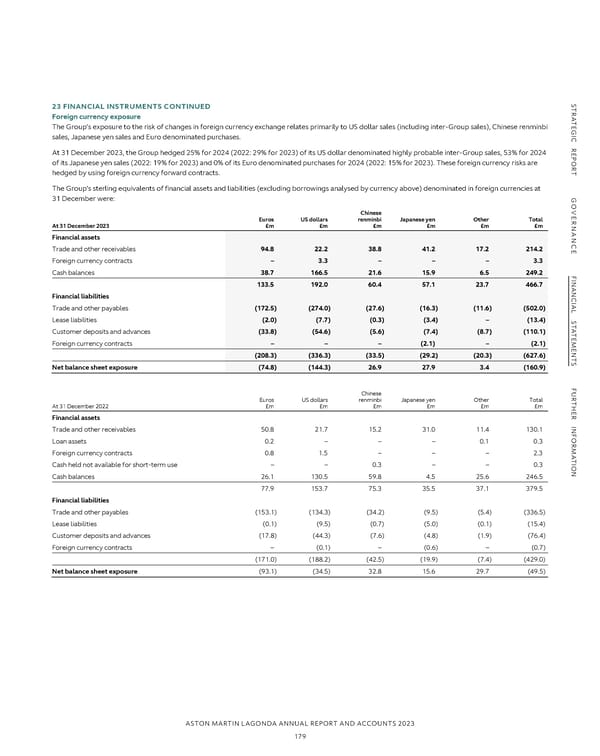

NOTES TO THE FINANCIAL STATEMENTS CONTINUED S S 23 FINANCIAL INSTRUMENTS CONTINUED TR23 FINANCIAL INSTRUMENTS CONTINUED TR Borrowings continued AForeign currency exposure A Derivative option over own shares continued TEThe Group’s exposure to the risk of changes in foreign currency exchange relates primarily to US dollar sales (including inter-Group sales), Chinese renminbi TE G G I I The warrants can be exercised from 1 July 2021 through to 7 December 2027. The issuance of debt with attached warrants required the Group to assess Csales, Japanese yen sales and Euro denominated purchases. C separately the fair value of the warrants and the debt. The fair value of the warrants was determined using a binomial model used to predict the behaviour R R E At 31 December 2023, the Group hedged 25% for 2024 (2022: 29% for 2023) of its US dollar denominated highly probable inter-Group sales, 53% for 2024 E of the warrant holders and when they might exercise their holdings. The derivative option liability was initially recognised as a derivative forward at fair value P P O of its Japanese yen sales (2022: 19% for 2023) and 0% of its Euro denominated purchases for 2024 (2022: 15% for 2023). These foreign currency risks are O with changes in the fair value being recognised in the Consolidated Income Statement until issuance of the warrants on 7 December 2020 resulting in an R R initial valuation of £34.6m. Upon issuance of the $335m SSNs, the carrying value of the debt was reduced by the same amount. The debt will be increased Thedged by using foreign currency forward contracts. T via an effective interest charge over the term of the SSNs. During the year ended 31 December 2023, changes to the fair value of the derivative option have The Group’s sterling equivalents of financial assets and liabilities (excluding borrowings analysed by currency above) denominated in foreign currencies at resulted in a debit to the Consolidated Income Statement of £19.0m (2022: £8.4m credit to the Consolidated Income Statement) which is presented in G31 December were: G adjusting items. A total of 29,969,927 (2022: nil warrants) were exercised, resulting in a £18.6m reduction to the liability (2022: no change to the associated O O liability). VE Chinese VE R Euros US dollars renminbi Japanese yen Other Total R NAN At 31 December 2023 £m £m £m £m £m £m NAN Interest rate risk Financial assets C C The Group is exposed interest rate risk on the RCF attached to the SSNs and on the bilateral RCF facility with HSBC when drawn, whereby Chinese renminbi ETrade and other receivables 94.8 22.2 38.8 41.2 17.2 214.2 E have been deposited in a restricted account with HSBC in China in exchange for a sterling overdraft facility with HSBC in the UK. The interest rate charged on Foreign currency contracts – 3.3 – – – 3.3 both facilities is based on SONIA and compounded in arrears. Cash balances 38.7 166.5 21.6 15.9 6.5 249.2 F F I I Profile NAN 133.5 192.0 60.4 57.1 23.7 466.7 NAN At 31 December the interest rate profile of the Group’s interest-bearing financial instruments was: C Financial liabilities C 2023 2022 IAL Trade and other payables (172.5) (274.0) (27.6) (16.3) (11.6) (502.0) IAL £m £m S Lease liabilities (2.0) (7.7) (0.3) (3.4) – (13.4) S Fixed rate instruments T T A A T Customer deposits and advances (33.8) (54.6) (5.6) (7.4) (8.7) (110.1) T Financial liabilities 980.3 1,104.0 E E M Foreign currency contracts – – – (2.1) – (2.1) M E E N (208.3) (336.3) (33.5) (29.2) (20.3) (627.6) N T T Variable rate instruments SNet balance sheet exposure (74.8) (144.3) 26.9 27.9 3.4 (160.9) S Financial liabilities 89.4 107.1 F F U Chinese U The SSNs, are at fixed interest rates. The rate of interest on the RCF, which is attached to the SSNs, and the bilateral RCF are based on SONIA plus a R R T Euros US dollars renminbi Japanese yen Other Total T percentage spread. As SONIA varies on a daily basis both the RCF and bilateral RCF are considered to be variable rate instruments. The bilateral is now HAt 31 December 2022 £m £m £m £m £m £m H E E drawn as at 31 December 2023. R R Financial assets INF Trade and other receivables 50.8 21.7 15.2 31.0 11.4 130.1 INF In 2023 and 2022, the Group entered into an inventory repurchase arrangement (not included within the financial liabilities noted above). The interest OR OR charged on this arrangement is determined as the difference between the sales and repurchase value and is therefore fixed at the time of entering into Loan assets 0.2 – – – 0.1 0.3 the arrangement. The repayment terms of this arrangement are not in excess of 270 days. M M A A Foreign currency contracts 0.8 1.5 – – – 2.3 T T I I Surplus cash funds, when appropriate, are placed on deposit and attract interest at variable rates. ONCash held not available for short-term use – – 0.3 – – 0.3 ON Interest rate risks – sensitivity Cash balances 26.1 130.5 59.8 4.5 25.6 246.5 The following table demonstrates the sensitivity, with all other variables held constant, of the Group’s loss after tax to a reasonably possible change in 77.9 153.7 75.3 35.5 37.1 379.5 interest rates on the bilateral RCF with HSBC and the RCF attached to the SSNs. Financial liabilities 2023 2022 Trade and other payables (153.1) (134.3) (34.2) (9.5) (5.4) (336.5) £m £m Lease liabilities (0.1) (9.5) (0.7) (5.0) (0.1) (15.4) Increase/ Effect Effect Customer deposits and advances (17.8) (44.3) (7.6) (4.8) (1.9) (76.4) (decrease) in on loss on loss interest rate after tax after tax Foreign currency contracts – (0.1) – (0.6) – (0.7) SONIA (3.0%) (2.1) (2.6) (171.0) (188.2) (42.5) (19.9) (7.4) (429.0) SONIA 3.0% 2.1 2.6 Net balance sheet exposure (93.1) (34.5) 32.8 15.6 29.7 (49.5) ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 179

Annual Report and Accounts Page 180 Page 182

Annual Report and Accounts Page 180 Page 182