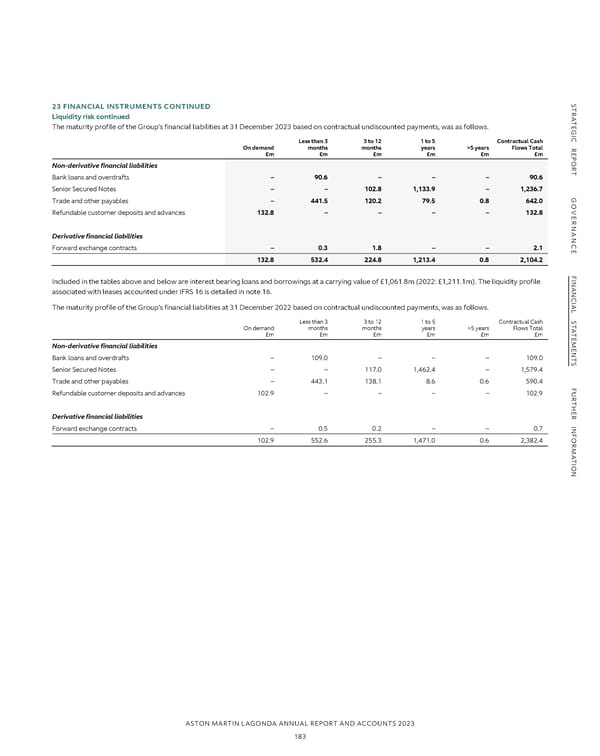

NOTES TO THE FINANCIAL STATEMENTS CONTINUED S S 23 FINANCIAL INSTRUMENTS CONTINUED TR23 FINANCIAL INSTRUMENTS CONTINUED TR Hedge accounting continued ALiquidity risk continued A Main sources of hedge ineffectiveness continued TEThe maturity profile of the Group’s financial liabilities at 31 December 2023 based on contractual undiscounted payments, was as follows. TE G G I I The effect of the cash flow hedge in the Consolidated Income Statement and Other Comprehensive Income is: C C R Less than 3 3 to 12 1 to 5 Contractual Cash R On demand months months years >5 years Flows Total Amount E £m £m £m £m £m £m E Total hedging Ineffectiveness Fair value reclassified P P (loss)/gain recognised in the movement from OCI to O O R Non-derivative financial liabilities R recognised Income Income on cash flow the Income Income T T in OCI Statement Statement hedges Statement Statement Bank loans and overdrafts – 90.6 – – – 90.6 Year ended 31 December 2023 £m £m line item £m £m line item Senior Secured Notes – – 102.8 1,133.9 – 1,236.7 Foreign exchange forward contracts (0.8) – Cost of sales 0.7 (1.5) Cost of sales GTrade and other payables – 441.5 120.2 79.5 0.8 642.0 G $400m Senior Secured Notes – hedge instrument (3.9) – Cost of sales – (3.9) Cost of sales O O Tax on fair value movements recognised in OCI 1.2 – – (0.2) 1.4 – VERefundable customer deposits and advances 132.8 – – – – 132.8 VE R R NAN NAN Derivative financial liabilities Amount C C Total hedging Fair value reclassified EForward exchange contracts – 0.3 1.8 – – 2.1 E gain/(loss) Ineffectiveness movement from OCI to 132.8 532.4 224.8 1,213.4 0.8 2,104.2 recognised recognised in the Income on cash flow the Income Income in OCI Income Statement Statement hedges Statement Statement Year ended 31 December 2022 £m £m line item £m £m line item F F I I Foreign exchange forward contracts 1.7 (0.3) Cost of sales (6.1) 7.8 Cost of sales NANIncluded in the tables above and below are interest bearing loans and borrowings at a carrying value of £1,061.8m (2022: £1,211.1m). The liquidity profile NAN associated with leases accounted under IFRS 16 is detailed in note 16. $400m Senior Secured Notes – hedge instrument (4.9) – Cost of sales – (4.9) Cost of sales C C IAL The maturity profile of the Group’s financial liabilities at 31 December 2022 based on contractual undiscounted payments, was as follows. IAL Tax on fair value movements recognised in OCI 0.9 – – 1.5 (0.7) – S Less than 3 3 to 12 1 to 5 Contractual Cash S T T A On demand months months years >5 years Flows Total A Hedge ineffectiveness recognised within the Consolidated Income Statement relates to differences in the nominal value of the hedged items and the T £m £m £m £m £m £m T E E hedging instrument. At 31 December 2023 and 2022, there were no balances remaining in the cash flow hedge reserve from hedging relationships for M M Non-derivative financial liabilities E E which hedge accounting is no longer required. N N T Bank loans and overdrafts – 109.0 – – – 109.0 T All hedging instruments recognised by the Group at 31 December 2023 have a maturity date of less than one year. S S Senior Secured Notes – – 117.0 1,462.4 – 1,579.4 Liquidity risk Trade and other payables – 443.1 138.1 8.6 0.6 590.4 F F U U The Group seeks to manage liquidity risk to ensure sufficient liquidity is available to meet foreseeable needs and, when appropriate, allow placement of Refundable customer deposits and advances 102.9 – – – – 102.9 R R T T H H cash on deposit safely and profitably. During 2023, the Group undertook a share placing and retail offer to strengthen the liquidity of the business. E E R R Derivative financial liabilities At 31 December 2022, the Group had entered into a bilateral revolving credit facility with HSBC Bank plc (“HSBC”), whereby Chinese Renminbi were INFForward exchange contracts – 0.5 0.2 – – 0.7 INF deposited in a restricted account with HSBC in China in exchange for a £30.0m Sterling overdraft facility with HSBC Bank plc in the United Kingdom. The OR OR restricted cash was revalued at 31 December 2022 to £32.8m and is shown in the cash and cash equivalents. At 31 December 2022, the facility of £30.0m 102.9 552.6 255.3 1,471.0 0.6 2,382.4 was shown within borrowings in current liabilities on the Statement of Financial Position. During the year ended 31 December 2023, the bilateral revolving M M A A credit facility was repaid. The facility remains available until 31 August 2025 and the total facility size is £50m. T T I I ON ON At 31 December 2023 the Group held £972.7m of SSNs (2022: £1,104.0m). In November 2023, the Group repurchased $121.7m of Second Lien SSNs. In October 2022 the Group repurchased $40.3m of First Lien SSNs and $143.8m of Second Lien SSNs. The premium paid on redemption was £8.0m (2022: £14.3m). The First Lien Notes are repayable in November 2025 and the Second Lien Notes in November 2026. The portion of unamortised fees and the redemption premium was charged to the Consolidated Income Statement at the point of redemption as an accelerated charge and presented within adjusting items (note 5). Transaction costs of £Nil (2022: £1.9m) relating to the repurchase are included in adjusting items (note 5). The US dollar amounts have been converted to sterling equivalents for reporting purposes. Attached to the SSNs is a £99.6m (2022: £90.6m) RCF of which £90.0m (2022: £78.5m) was drawn in cash at the reporting date. The amount recorded in the Statement of Financial Position is net of unamortised transaction costs. £4.4m (2022: £5.2m) of the remaining ancillary facility has been utilised through the issuance of letters of credit and guarantees. The RCF attached to the SSNs is available until August 2025. As part of the normal operating cycle of the Group, customers make advanced payments to secure their allocation of Special Vehicles produced in limited numbers. The cash from these advance payments is primarily used to fund upfront costs of the Special Vehicle project, including raw materials and components required in manufacture. In certain circumstances, according to the individual terms of the Special Vehicle contract and the position of the customer in the staged deposit and vehicle specification process, the advanced payments are contractually refundable. At 31 December 2023, the Group held refundable deposits of £132.8m (2022: £102.9m). The Special Vehicle programmes are typically oversubscribed and, in the event that a customer requests reimbursement of their advanced payment, the newly created allocation is then given to an alternative customer, who is required to make an equivalent advanced payment. ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 183

Annual Report and Accounts Page 184 Page 186

Annual Report and Accounts Page 184 Page 186