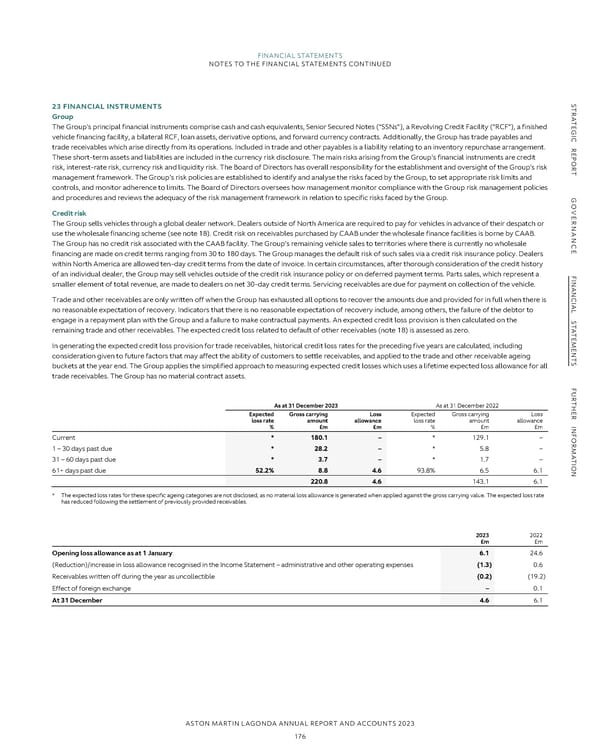

FFIINANNANCCIALIAL S STTAATTEEMMEENNTTSS NOTES TO THE FINANCIAL STATEMENTS CONTINUED S 23 FINANCIAL INSTRUMENTS TR Group A The Group's principal financial instruments comprise cash and cash equivalents, Senior Secured Notes (“SSNs”), a Revolving Credit Facility (“RCF”), a finished TE G I vehicle financing facility, a bilateral RCF, loan assets, derivative options, and forward currency contracts. Additionally, the Group has trade payables and C trade receivables which arise directly from its operations. Included in trade and other payables is a liability relating to an inventory repurchase arrangement. R E These short-term assets and liabilities are included in the currency risk disclosure. The main risks arising from the Group's financial instruments are credit P O risk, interest-rate risk, currency risk and liquidity risk. The Board of Directors has overall responsibility for the establishment and oversight of the Group's risk R management framework. The Group's risk policies are established to identify and analyse the risks faced by the Group, to set appropriate risk limits and T controls, and monitor adherence to limits. The Board of Directors oversees how management monitor compliance with the Group risk management policies and procedures and reviews the adequacy of the risk management framework in relation to specific risks faced by the Group. G O Credit risk VE The Group sells vehicles through a global dealer network. Dealers outside of North America are required to pay for vehicles in advance of their despatch or R use the wholesale financing scheme (see note 18). Credit risk on receivables purchased by CAAB under the wholesale finance facilities is borne by CAAB. NAN The Group has no credit risk associated with the CAAB facility. The Group’s remaining vehicle sales to territories where there is currently no wholesale C financing are made on credit terms ranging from 30 to 180 days. The Group manages the default risk of such sales via a credit risk insurance policy. Dealers E within North America are allowed ten-day credit terms from the date of invoice. In certain circumstances, after thorough consideration of the credit history of an individual dealer, the Group may sell vehicles outside of the credit risk insurance policy or on deferred payment terms. Parts sales, which represent a F I smaller element of total revenue, are made to dealers on net 30-day credit terms. Servicing receivables are due for payment on collection of the vehicle. NAN Trade and other receivables are only written off when the Group has exhausted all options to recover the amounts due and provided for in full when there is C no reasonable expectation of recovery. Indicators that there is no reasonable expectation of recovery include, among others, the failure of the debtor to IAL engage in a repayment plan with the Group and a failure to make contractual payments. An expected credit loss provision is then calculated on the S T remaining trade and other receivables. The expected credit loss related to default of other receivables (note 18) is assessed as zero. A T E In generating the expected credit loss provision for trade receivables, historical credit loss rates for the preceding five years are calculated, including M E N consideration given to future factors that may affect the ability of customers to settle receivables, and applied to the trade and other receivable ageing T buckets at the year end. The Group applies the simplified approach to measuring expected credit losses which uses a lifetime expected loss allowance for all S trade receivables. The Group has no material contract assets. F U R T As at 31 December 2023 As at 31 December 2022 H E Expected Gross carrying Loss Expected Gross carrying Loss R loss rate amount allowance loss rate amount allowance INF % £m £m % £m £m OR Current * 180.1 – * 129.1 – M 1 – 30 days past due * 28.2 – * 5.8 – A T 31 – 60 days past due * 3.7 – * 1.7 – I ON 61+ days past due 52.2% 8.8 4.6 93.8% 6.5 6.1 220.8 4.6 143.1 6.1 * The expected loss rates for these specific ageing categories are not disclosed, as no material loss allowance is generated when applied against the gross carrying value. The expected loss rate has reduced following the settlement of previously provided receivables. 2023 2022 £m £m Opening loss allowance as at 1 January 6.1 24.6 (Reduction)/increase in loss allowance recognised in the Income Statement – administrative and other operating expenses (1.3) 0.6 Receivables written off during the year as uncollectible (0.2) (19.2) Effect of foreign exchange – 0.1 At 31 December 4.6 6.1 ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 176

Annual Report and Accounts Page 177 Page 179

Annual Report and Accounts Page 177 Page 179