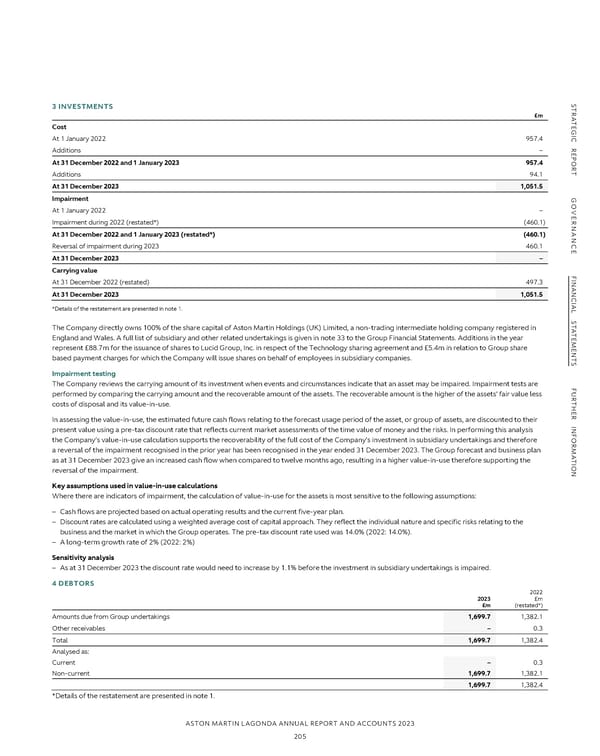

NOTES TO THE PARENT COMPANY FINANCIAL STATEMENTS CONTINUED S S Prior year restatement TR3 INVESTMENTS TR Following a review by the Financial Reporting Council (“FRC”), the Company revisited its assumptions used in determining the recoverability of the carrying A £m A value of the investment in subsidiaries. The original assessment had not considered the recoverability of the intercompany balances within the Company TECost TE G G I I prior to assessing the recoverability of the investment valuation. When updating for this assumption, the net recoverable value of the investment is reduced CAt 1 January 2022 957.4 C from £957.4m to £497.3m at 31 December 2022. The impairment of £460.1m is reflected in the Parent Company Income Statement for the prior year. RAdditions – R E E P P O At 31 December 2022 and 1 January 2023 957.4 O As part of the same review it was identified the intercompany receivable was presented as current, however, the Company did not expect to receive R R repayment within 12 months from the balance sheet date. The intercompany receivable balance has therefore been restated as a non-current asset in the TAdditions 94.1 T prior year Company Balance Sheet. In addition, the Expected Credit Loss provision recognised against the intercompany receivable is deemed not required. At 31 December 2023 1,051.5 This is due to the balance being intercompany in nature and the parent company can allow the benefit of time to its subsidiary in order to recover the GImpairment G receivable in full from the future cashflows of the subsidiary. As there is no anticipated shortfall in repayment of the receivable over time, no expected O O credit loss provision is required. An opening reserves adjustment of £36.0m is made to reflect removing the provision as at 1 January 2022. A £11.2m charge VEAt 1 January 2022 – VE R Impairment during 2022 (restated*) (460.1) R is reflected in the Income Statement for the year ended 31 December 2022, reflecting the movement in the provision previously recognised between NANAt 31 December 2022 and 1 January 2023 (restated*) (460.1) NAN 1 January 2022 and 31 December 2022. C Reversal of impairment during 2023 460.1 C The restatements noted above have no impact on the previous, current or future results of the Group. The FRC’s review does not benefit from detailed EAt 31 December 2023 – E knowledge of our business or an understanding of the underlying transactions entered into and therefore provides no assurance that the Annual Report Carrying value F F is correct in all material aspects. I I NAN At 31 December 2022 (restated) 497.3 NAN At 31 December 2023 1,051.5 C C IAL *Details of the restatement are presented in note 1. IAL As previously reported Adjustment Restated balance S S 31 December 2022 31 December 2022 T T Liabilities £m £m £m AThe Company directly owns 100% of the share capital of Aston Martin Holdings (UK) Limited, a non-trading intermediate holding company registered in A T T E England and Wales. A full list of subsidiary and other related undertakings is given in note 33 to the Group Financial Statements. Additions in the year E M M Non-current assets E represent £88.7m for the issuance of shares to Lucid Group, Inc. in respect of the Technology sharing agreement and £5.4m in relation to Group share E N N Investments 957.4 (460.1) 497.3 T based payment charges for which the Company will issue shares on behalf of employees in subsidiary companies. T Debtors: amounts falling due in more than one year – 1,382.1 1,382.1 S S Impairment testing The Company reviews the carrying amount of its investment when events and circumstances indicate that an asset may be impaired. Impairment tests are F F Current assets U performed by comparing the carrying amount and the recoverable amount of the assets. The recoverable amount is the higher of the assets’ fair value less U R R Debtors: amounts falling due within one year 1,357.6 (1,357.3) 0.3 T T H costs of disposal and its value-in-use. H E E R R INF In assessing the value-in-use, the estimated future cash flows relating to the forecast usage period of the asset, or group of assets, are discounted to their INF Capital and reserves present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks. In performing this analysis OR OR Retained Earnings 179.0 (435.3) (256.3) the Company’s value-in-use calculation supports the recoverability of the full cost of the Company’s investment in subsidiary undertakings and therefore M M a reversal of the impairment recognised in the prior year has been recognised in the year ended 31 December 2023. The Group forecast and business plan A A The loss on ordinary activities after taxation amounts to £454.1m (previously reported profit of £17.2m). Tas at 31 December 2023 give an increased cash flow when compared to twelve months ago, resulting in a higher value-in-use therefore supporting the T I I ON reversal of the impairment. ON As previously reported 1 Adjustment Restated balance Key assumptions used in value-in-use calculations January 2022 1 January 2022 Where there are indicators of impairment, the calculation of value-in-use for the assets is most sensitive to the following assumptions: Liabilities £m £m £m Non-current assets – Cash flows are projected based on actual operating results and the current five-year plan. Debtors: amounts falling due in more than one year – 749.7 749.7 – Discount rates are calculated using a weighted average cost of capital approach. They reflect the individual nature and specific risks relating to the business and the market in which the Group operates. The pre-tax discount rate used was 14.0% (2022: 14.0%). – A long-term growth rate of 2% (2022: 2%) Current assets Debtors: amounts falling due within one year 713.7 (713.7) – Sensitivity analysis – As at 31 December 2023 the discount rate would need to increase by 1.1% before the investment in subsidiary undertakings is impaired. Capital and reserves 4 DEBTORS Retained Earnings 161.8 36.0 197.8 2022 2023 £m £m (restated*) Amounts due from Group undertakings 1,699.7 1,382.1 The profit on ordinary activities after taxation amounts to £70.9m (previously reported profit of £34.9m). Other receivables – 0.3 Total 1,699.7 1,382.4 Analysed as: 2 DIRECTORS’ REMUNERATION Current – 0.3 The Company has no employees other than the Directors. Full details of the Directors’ remuneration is given in the Directors’ Remuneration Report. Non-current 1,699.7 1,382.1 1,699.7 1,382.4 *Details of the restatement are presented in note 1. ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 205

Annual Report and Accounts Page 206 Page 208

Annual Report and Accounts Page 206 Page 208