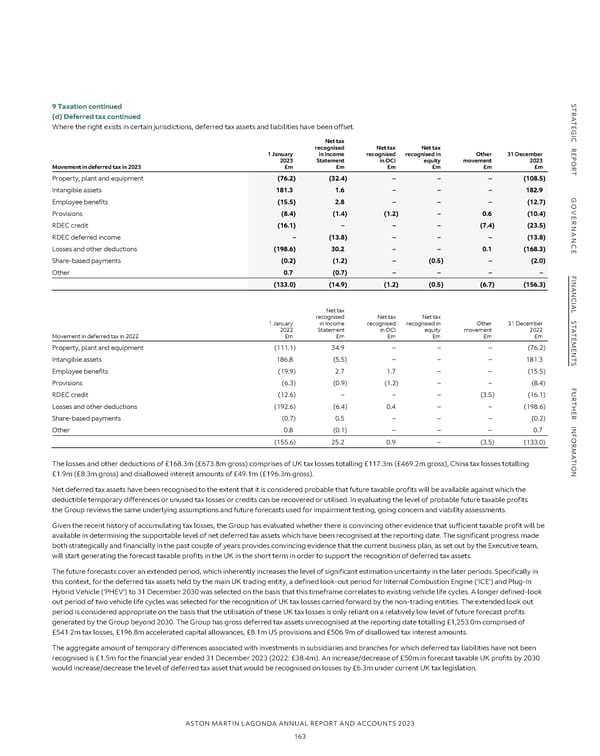

NOTES TO THE FINANCIAL STATEMENTS CONTINUED S S 9 TAXATION CONTINUED TR 9 Taxation continued TR (a) Reconciliation of the total income tax (credit)/charge A(d) Deferred tax continued A The tax credit (2022: charge) in the Consolidated Statement of Comprehensive Income for the year is lower (2022: higher) than the standard rate of TEWhere the right exists in certain jurisdictions, deferred tax assets and liabilities have been offset. TE G G I I corporation tax in the UK of 23.5% (2022: 19%). The differences are reconciled below: C C R Net tax R recognised Net tax Net tax 2023 2022 E 1 January in Income recognised recognised in Other 31 December E £m £m P P O 2023 Statement in OCI equity movement 2023 O Loss from operations before taxation (239.8) (495.0) RMovement in deferred tax in 2023 £m £m £m £m £m £m R Loss from operations before taxation multiplied by standard rate of corporation tax in the UK of 23.5% (2022: 19.0%) (56.3) (94.0) TProperty, plant and equipment (76.2) (32.4) – – – (108.5) T Difference to total income tax (credit)/charge due to effects of: Intangible assets 181.3 1.6 – – – 182.9 G G Expenses not deductible for tax purposes 1.2 2.0 OEmployee benefits (15.5) 2.8 – – – (12.7) O Movement in unprovided deferred tax 43.4 100.3 VEProvisions (8.4) (1.4) (1.2) – 0.6 (10.4) VE R R Derecognition of deferred tax assets – 25.6 NANRDEC credit (16.1) – – – (7.4) (23.5) NAN Irrecoverable overseas withholding taxes – 0.8 RDEC deferred income – (13.8) – – – (13.8) C C Adjustments in respect of prior periods 0.1 (4.3) ELosses and other deductions (198.6) 30.2 – – 0.1 (168.3) E Difference in UK tax rates (0.7) 1.1 Share-based payments (0.2) (1.2) – (0.5) – (2.0) Other 0.7 (0.7) – – – – Difference in overseas tax rates 0.2 1.2 F F I I Other (0.9) – NAN (133.0) (14.9) (1.2) (0.5) (6.7) (156.3) NAN Total income tax (credit)/charge (13.0) 32.7 C C IAL Net tax IAL S recognised Net tax Net tax S (b) Tax paid T 1 January in Income recognised recognised in Other 31 December T A 2022 Statement in OCI equity movement 2022 A Total net tax paid during the year was £5.6m (2022: £6.8m). T T E Movement in deferred tax in 2022 £m £m £m £m £m £m E M M (c) Factors affecting future tax charges E E Property, plant and equipment (111.1) 34.9 – – – (76.2) N N The UK’s main rate of corporation tax increased from 19% to 25%, effective from 1 April 2023. TIntangible assets 186.8 (5.5) – – – 181.3 T S Employee benefits (19.9) 2.7 1.7 – – (15.5) S Pillar Two legislation has been enacted or substantively enacted in certain jurisdictions in which the Group operates. The legislation will be effective for the Group's financial year beginning 1 January 2024. The Group has performed an assessment of the Group's potential exposure to Pillar Two income taxes. Provisions (6.3) (0.9) (1.2) – – (8.4) F F The assessment of the potential exposure to Pillar Two income taxes is based on the most recent tax filings, country-by-country reporting and financial URDEC credit (12.6) – – – (3.5) (16.1) U R R statements for the constituent entities in the Group. Based on the assessment, the Pillar Two Transitional Safe Harbour provisions are expected to apply in T T H Losses and other deductions (192.6) (6.4) 0.4 – – (198.6) H each jurisdiction the Group operates in, and management is not aware of any circumstance under which this might change. Therefore, the Group does not E E R R expect a potential exposure to Pillar Two top-up taxes. The Group has applied the exception in IAS 12 ’Income Taxes’ to recognising and disclosing INFShare-based payments (0.7) 0.5 – – – (0.2) INF information about deferred tax assets and liabilities related to Pillar Two income taxes. Other 0.8 (0.1) – – – 0.7 OR OR (155.6) 25.2 0.9 – (3.5) (133.0) (d) Deferred tax M M A A Recognised deferred tax assets and liabilities. T T I I ON The losses and other deductions of £168.3m (£673.8m gross) comprises of UK tax losses totalling £117.3m (£469.2m gross), China tax losses totalling ON Deferred tax assets and liabilities are attributable to the following: £1.9m (£8.3m gross) and disallowed interest amounts of £49.1m (£196.3m gross). Assets Assets Liabilities Liabilities Net deferred tax assets have been recognised to the extent that it is considered probable that future taxable profits will be available against which the 2023 2022 2023 2022 deductible temporary differences or unused tax losses or credits can be recovered or utilised. In evaluating the level of probable future taxable profits £m £m £m £m Property, plant and equipment (108.5) (76.2) – – the Group reviews the same underlying assumptions and future forecasts used for impairment testing, going concern and viability assessments. Intangible assets – – 182.9 181.3 Given the recent history of accumulating tax losses, the Group has evaluated whether there is convincing other evidence that sufficient taxable profit will be Employee benefits (12.7) (15.5) – – available in determining the supportable level of net deferred tax assets which have been recognised at the reporting date. The significant progress made Provisions (10.4) (8.4) – – both strategically and financially in the past couple of years provides convincing evidence that the current business plan, as set out by the Executive team, 1 will start generating the forecast taxable profits in the UK in the short term in order to support the recognition of deferred tax assets. RDEC credit (23.5) (16.1) – – 2 The future forecasts cover an extended period, which inherently increases the level of significant estimation uncertainty in the later periods. Specifically in RDEC deferred income (13.8) – – 3 this context, for the deferred tax assets held by the main UK trading entity, a defined look-out period for Internal Combustion Engine (‘ICE’) and Plug-In Losses and other deductions (168.3) (198.6) – – Share-based payments (2.0) (0.2) – – Hybrid Vehicle (‘PHEV’) to 31 December 2030 was selected on the basis that this timeframe correlates to existing vehicle life cycles. A longer defined-look Other – – – 0.7 out period of two vehicle life cycles was selected for the recognition of UK tax losses carried forward by the non-trading entities. The extended look out period is considered appropriate on the basis that the utilisation of these UK tax losses is only reliant on a relatively low level of future forecast profits Deferred tax (assets)/liabilities (339.2) (315.0) 182.9 182.0 generated by the Group beyond 2030. The Group has gross deferred tax assets unrecognised at the reporting date totalling £1,253.0m comprised of Offset of tax liabilities/(assets) 182.9 181.3 (182.9) (181.3) £541.2m tax losses, £196.8m accelerated capital allowances, £8.1m US provisions and £506.9m of disallowed tax interest amounts. Total deferred tax (assets)/liabilities (156.3) (133.7) – 0.7 The aggregate amount of temporary differences associated with investments in subsidiaries and branches for which deferred tax liabilities have not been 1 Deferred tax assets categorised as ‘RDEC credit’ relate to the cumulative restricted amount of the payable tax credits which can be applied or surrendered in discharging any future corporation recognised is £1.5m for the financial year ended 31 December 2023 (2022: £38.4m). An increase/decrease of £50m in forecast taxable UK profits by 2030 tax liability of the claimant company, as detailed in the Government Grants section of the Accounting Policies (Note 2). would increase/decrease the level of deferred tax asset that would be recognised on losses by £6.3m under current UK tax legislation. 2 Deferred tax assets categorised as ‘RDEC deferred income’ relate to expenditure deferred to the Consolidated Statement of Financial position which has previously been included within filed RDEC claims and subject to corporation tax. Any future release of the RDEC deferred income to the Consolidated Income Statement will not be subject to corporation tax for a second time. 3 Deferred tax assets categorised as ‘Losses and other deductions’ relate to tax losses and tax interest amounts disallowed under the corporate interest restriction legislation. ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 163

Annual Report and Accounts Page 164 Page 166

Annual Report and Accounts Page 164 Page 166