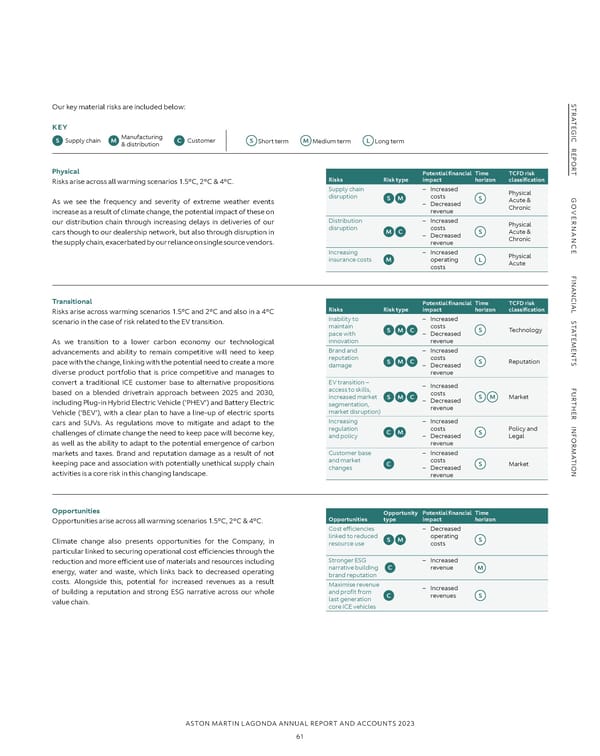

S S TR Our key material risks are included below: TR A A TE KEY TE G G I I C Manufacturing C R S Supply chain M C Customer R S Short term M Medium term L Long term & distribution E E P P O O R R T Physical Potential financial Time TCFD risk T Risks arise across all warming scenarios 1.5°C, 2°C & 4°C. Risks Risk type impact horizon classification Supply chain – Increased Physical G disruption S M costs G S Acute & O As we see the frequency and severity of extreme weather events – Decreased Chronic O VE increase as a result of climate change, the potential impact of these on revenue VE R our distribution chain through increasing delays in deliveries of our Distribution – Increased R NAN disruption M C costs Physical NAN cars though to our dealership network, but also through disruption in – Decreased S Acute & Chronic C the supply chain, exacerbated by our reliance on single source vendors. revenue C E Increasing – Increased Physical E insurance costs M operating L Acute costs F F I I NAN NAN C C IAL Transitional Potential financial Time TCFD risk IAL Risks Risk type impact horizon classification S Risks arise across warming scenarios 1.5°C and 2°C and also in a 4°C Inability to – Increased S T scenario in the case of risk related to the EV transition. maintain costs T A Technology A S M C S T pace with – Decreased T E E M As we transition to a lower carbon economy our technological innovation revenue M E E N advancements and ability to remain competitive will need to keep Brand and – Increased N T reputation costs T S Reputation S pace with the change, linking with the potential need to create a more damage S M C – Decreased S diverse product portfolio that is price competitive and manages to revenue convert a traditional ICE customer base to alternative propositions EV transition – – Increased F access to skills, F U based on a blended drivetrain approach between 2025 and 2030, costs U R increased market Market R S M C S M T including Plug-in Hybrid Electric Vehicle (‘PHEV’) and Battery Electric – Decreased T H segmentation, revenue H E Vehicle (‘BEV’), with a clear plan to have a line-up of electric sports market disruption) E R R INF cars and SUVs. As regulations move to mitigate and adapt to the Increasing – Increased INF regulation C M costs Policy and challenges of climate change the need to keep pace will become key, and policy – Decreased S Legal OR as well as the ability to adapt to the potential emergence of carbon revenue OR M M A markets and taxes. Brand and reputation damage as a result of not Customer base – Increased A T and market costs T I keeping pace and association with potentially unethical supply chain C Market I ON activities is a core risk in this changing landscape. changes – Decreased S ON revenue Opportunities Opportunity Potential financial Time Opportunities arise across all warming scenarios 1.5°C, 2°C & 4°C. Opportunities type impact horizon Cost efÏciencies – Decreased linked to reduced S M operating Climate change also presents opportunities for the Company, in resource use costs S particular linked to securing operational cost efÏciencies through the Stronger ESG – Increased reduction and more efÏcient use of materials and resources including narrative building C revenue energy, water and waste, which links back to decreased operating M brand reputation costs. Alongside this, potential for increased revenues as a result Maximise revenue – Increased of building a reputation and strong ESG narrative across our whole and profit from C revenues value chain. last generation S core ICE vehicles ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 61

Annual Report and Accounts Page 62 Page 64

Annual Report and Accounts Page 62 Page 64