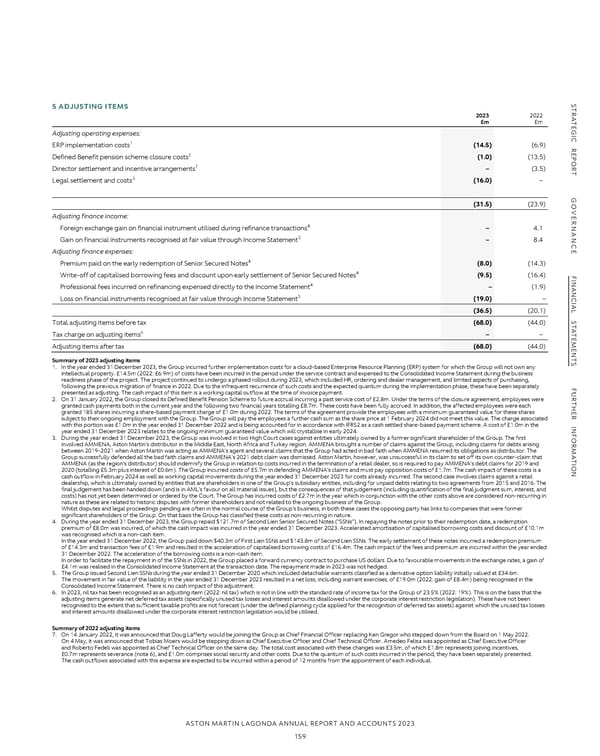

NOTES TO THE FINANCIAL STATEMENTS CONTINUED S S 4 OPERATING LOSS TR 5 ADJUSTING ITEMS TR The Group’s operating loss is stated after charging/(crediting): A 2023 2022 A TE £m £m TE 2023 2022 G Adjusting operating expenses: G I I £m £m C C R 1 R Depreciation of property, plant and equipment (note 14) 91.2 80.7 ERP implementation costs (14.5) (6.9) E 2 E P Defined Benefit pension scheme closure costs (1.0) (13.5) P Depreciation absorbed into inventory under standard costing (0.9) (2.9) O O R 7 R Loss on sale/scrap of property, plant and equipment 2.6 – TDirector settlement and incentive arrangements – (3.5) T 3 Depreciation of right-of-use lease assets (note 16) 9.3 11.0 Legal settlement and costs (16.0) – Amortisation of intangible assets (note 12) 280.4 227.4 G G Amortisation released from/(absorbed into) inventory under standard costing 3.0 (8.1) O (31.5) (23.9) O VE Adjusting finance income: VE Depreciation, amortisation and impairment charges included in administrative and other operating expenses 385.6 308.1 R R NAN 4 NAN Foreign exchange gain on financial instrument utilised during refinance transactions – 4.1 5 Gain on financial instruments recognised at fair value through Income Statement – 8.4 (Decrease)/increase in trade receivable loss allowance – administrative and other operating expenses (note 23) (1.3) 0.6 C C Research and development expenditure tax credit (23.8) (18.4) EAdjusting finance expenses: E 4 Net foreign currency differences 0.3 8.7 Premium paid on the early redemption of Senior Secured Notes (8.0) (14.3) 4 F Write-off of capitalised borrowing fees and discount upon early settlement of Senior Secured Notes (9.5) (16.4) F Cost of inventories recognised as an expense 844.0 798.0 I I NAN 4 NAN Write-down of inventories to net realisable value 24.2 8.9 Professional fees incurred on refinancing expensed directly to the Income Statement – (1.9) C 5 C Loss on financial instruments recognised at fair value through Income Statement (19.0) – Increase in fair value of other derivative contracts (11.2) (2.3) IAL (36.5) (20.1) IAL Lease payments (gross of sub-lease receipts) S S Plant, machinery and IT equipment* 0.3 0.7 TTotal adjusting items before tax (68.0) (44.0) T A A T 6 T Tax charge on adjusting items – – Sub-lease receipts Land and buildings (0.4) (0.6) E E M M Auditor’s remuneration: EAdjusting items after tax (68.0) (44.0) E N N T Summary of 2023 adjusting items T Audit of these Financial Statements 0.3 0.3 S1. In the year ended 31 December 2023, the Group incurred further implementation costs for a cloud-based Enterprise Resource Planning (ERP) system for which the Group will not own any S Audit of Financial Statements of subsidiaries pursuant to legislation 0.5 0.4 intellectual property. £14.5m (2022: £6.9m) of costs have been incurred in the period under the service contract and expensed to the Consolidated Income Statement during the business Audit-related assurance 0.1 0.1 readiness phase of the project. The project continued to undergo a phased rollout during 2023, which included HR, ordering and dealer management, and limited aspects of purchasing, F following the previous migration of finance in 2022. Due to the infrequent recurrence of such costs and the expected quantum during the implementation phase, these have been separately F U presented as adjusting. The cash impact of this item is a working capital outflow at the time of invoice payment. U Services related to corporate finance transactions – 0.2 R2. On 31 January 2022, the Group closed its Defined Benefit Pension Scheme to future accrual incurring a past service cost of £2.8m. Under the terms of the closure agreement, employees were R T T Research and development expenditure recognised as an expense 30.7 14.1 Hgranted cash payments both in the current year and the following two financial years totalling £8.7m. These costs have been fully accrued. In addition, the affected employees were each H E granted 185 shares incurring a share-based payment charge of £1.0m during 2022. The terms of the agreement provide the employees with a minimum guaranteed value for these shares E R R * Election taken by the Group to not recognise right-of-use lease assets and equivalent lease liabilities for short-term and low-value leases. INFsubject to their ongoing employment with the Group. The Group will pay the employees a further cash sum as the share price at 1 February 2024 did not meet this value. The charge associated INF with this portion was £1.0m in the year ended 31 December 2022 and is being accounted for in accordance with IFRS2 as a cash settled share-based payment scheme. A cost of £1.0m in the year ended 31 December 2023 relates to the ongoing minimum guaranteed value which will crystallise in early 2024. 2023 2022 OR 3. During the year ended 31 December 2023, the Group was involved in two High Court cases against entities ultimately owned by a former significant shareholder of the Group. The first OR involved AMMENA, Aston Martin’s distributor in the Middle East, North Africa and Turkey region. AMMENA brought a number of claims against the Group, including claims for debts arising £m £m M between 2019-2021 when Aston Martin was acting as AMMENA’s agent and several claims that the Group had acted in bad faith when AMMENA resumed its obligations as distributor. The M A Group successfully defended all the bad faith claims and AMMENA’s 2021 debt claim was dismissed. Aston Martin, however, was unsuccessful in its claim to set off its own counter-claim that A Total research and development expenditure 299.2 246.1 T T I AMMENA (as the region’s distributor) should indemnify the Group in relation to costs incurred in the termination of a retail dealer, so is required to pay AMMENA’s debt claims for 2019 and I Capitalised research and development expenditure (note 12) (268.5) (232.0) ON2020 (totalling £5.3m plus interest of £0.6m). The Group incurred costs of £5.7m in defending AMMENA’s claims and must pay opposition costs of £1.7m. The cash impact of these costs is a ON Research and development expenditure recognised as an expense 30.7 14.1 cash outflow in February 2024 as well as working capital movements during the year ended 31 December 2023 for costs already incurred. The second case involves claims against a retail dealership, which is ultimately owned by entities that are shareholders in one of the Group’s subsidiary entities, including for unpaid debts relating to two agreements from 2015 and 2016. The final judgement has been handed down (and is in AML’s favour on all material issues), but the consequences of that judgement (including quantification of the final judgment sum, interest, and costs) has not yet been determined or ordered by the Court. The Group has incurred costs of £2.7m in the year which in conjunction with the other costs above are considered non-recurring in nature as these are related to historic disputes with former shareholders and not related to the ongoing business of the Group. Whilst disputes and legal proceedings pending are often in the normal course of the Group’s business, in both these cases the opposing party has links to companies that were former significant shareholders of the Group. On that basis the Group has classified these costs as non-recurring in nature. 4. During the year ended 31 December 2023, the Group repaid $121.7m of Second Lien Senior Secured Notes (“SSNs”). In repaying the notes prior to their redemption date, a redemption premium of £8.0m was incurred, of which the cash impact was incurred in the year ended 31 December 2023. Accelerated amortisation of capitalised borrowing costs and discount of £10.1m was recognised which is a non-cash item. In the year ended 31 December 2022, the Group paid down $40.3m of First Lien SSNs and $143.8m of Second Lien SSNs. The early settlement of these notes incurred a redemption premium of £14.3m and transaction fees of £1.9m and resulted in the acceleration of capitalised borrowing costs of £16.4m. The cash impact of the fees and premium are incurred within the year ended 31 December 2022. The acceleration of the borrowing costs is a non-cash item. In order to facilitate the repayment in of the SSNs in 2022, the Group placed a forward currency contract to purchase US dollars. Due to favourable movements in the exchange rates, a gain of £4.1m was realised in the Consolidated Income Statement at the transaction date. The repayment made in 2023 was not hedged. 5. The Group issued Second Lien SSNs during the year ended 31 December 2020 which included detachable warrants classified as a derivative option liability initially valued at £34.6m. The movement in fair value of the liability in the year ended 31 December 2023 resulted in a net loss, including warrant exercises, of £19.0m (2022: gain of £8.4m) being recognised in the Consolidated Income Statement. There is no cash impact of this adjustment. 6. In 2023, nil tax has been recognised as an adjusting item (2022: nil tax) which is not in line with the standard rate of income tax for the Group of 23.5% (2022: 19%). This is on the basis that the adjusting items generate net deferred tax assets (specifically unused tax losses and interest amounts disallowed under the corporate interest restriction legislation). These have not been recognised to the extent that sufficient taxable profits are not forecast (under the defined planning cycle applied for the recognition of deferred tax assets) against which the unused tax losses and interest amounts disallowed under the corporate interest restriction legislation would be utilised. Summary of 2022 adjusting items 7. On 14 January 2022, it was announced that Doug Lafferty would be joining the Group as Chief Financial Officer replacing Ken Gregor who stepped down from the Board on 1 May 2022. On 4 May, it was announced that Tobias Moers would be stepping down as Chief Executive Officer and Chief Technical Officer. Amedeo Felisa was appointed as Chief Executive Officer and Roberto Fedeli was appointed as Chief Technical Officer on the same day. The total cost associated with these changes was £3.5m, of which £1.8m represents joining incentives, £0.7m represents severance (note 6), and £1.0m comprises social security and other costs. Due to the quantum of such costs incurred in the period, they have been separately presented. The cash outflows associated with this expense are expected to be incurred within a period of 12 months from the appointment of each individual. ASTON MARTIN LAGONDA ANNUAL REPORT AND ACCOUNTS 2023 159

Annual Report and Accounts Page 160 Page 162

Annual Report and Accounts Page 160 Page 162